Did you know that nearly 40% of New Year’s resolutions in 2024 are money related? Did you know that only 9% of New Year’s resolutions are actually completed? Great, me neither (until a few minutes ago when I googled it). Nevertheless, my goal as a financial coach is to help you be one of the 9%, whether you are a 1:1 client or reading some random ‘Your Money Mark’ guy’s blog.

The 8 topics below come from the most popular themes that I have witnessed from my clients since I started coaching in 2020. They are:

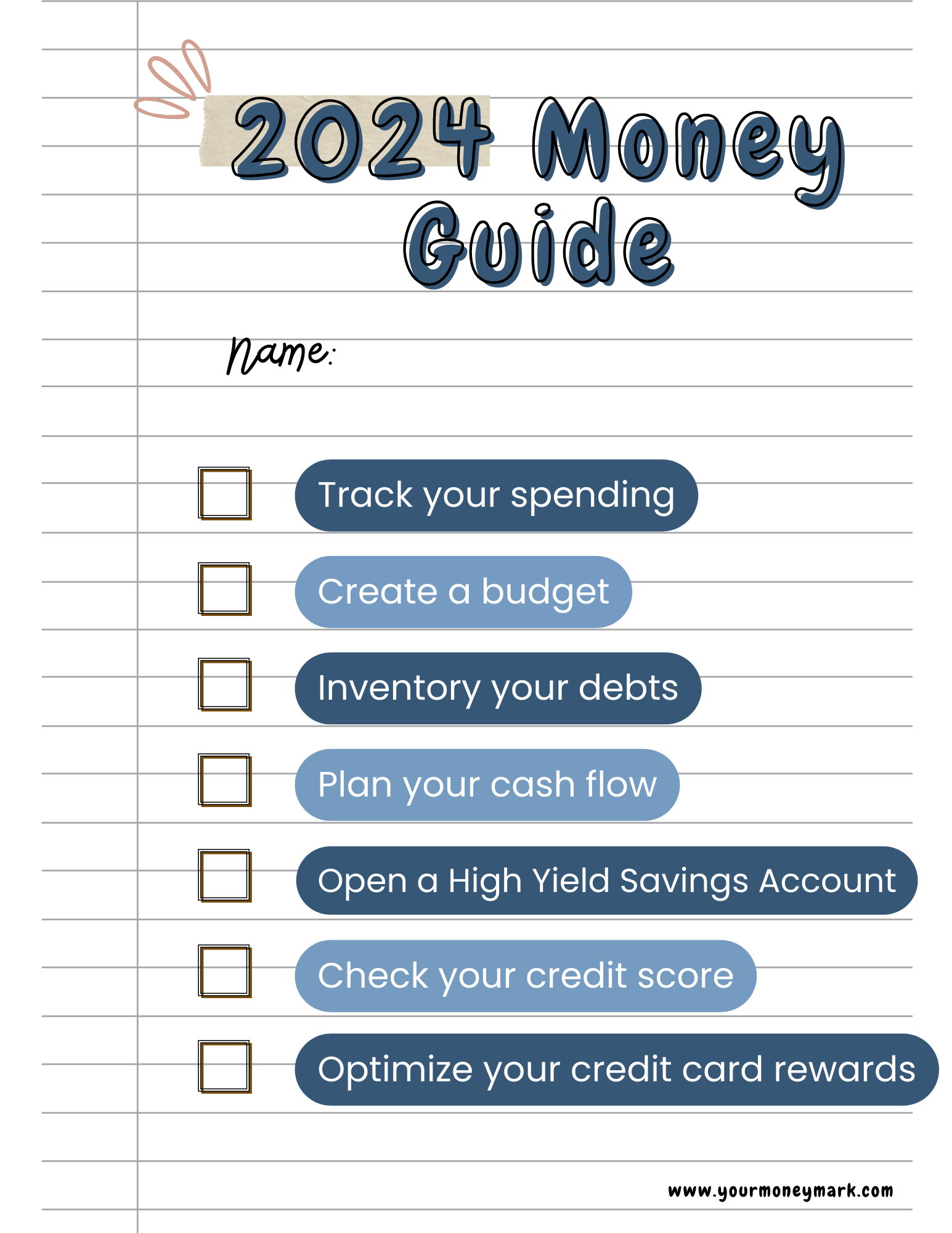

- Track your spending

- Create a budget

- Take inventory of your debts

- Plan your cash flow

- Open a High Yield Savings Account

- Check your credit score

- Optimize your credit card rewards

- Consolidate your retirement accounts

Track your spending

The first step in The 2024 Money Guide is by far the most important as it is the building block to personal finance. Track your spending.

There are dozens of ways to track spending, ranging from the envelope method, to personal finance apps, to a good ole’ excel spreadsheet. The main goal in this step is not to set a constricting budget but rather to understand where your money is going. I’ll be completely honest here – the easiest option, by far, is using an app that can track and categorize your spending automatically.

Create a budget

If you followed my advice with a personal finance app, this step should be pretty ingrained in the experience of the app. Creating a budget is the next step in The 2024 Money Guide. Now that you have an idea of where your unrestricted spend is going, it’s time to put some bounds on that spending. It’s imporant not to be too strict because you are trying to create a sustainable, habitual money mindset. So if you realize you are spending $600 on food, try cutting that back to $500 to start – you can always change to a more aggressive goal later!

The final outcome of your budget should be a somewhat predictable cash flow for the month. This figure is what you’ll use for funding whatever your 2024 money goals may be.

Take inventory of your debts

Now that you’ve determined your cash flow, it’s time to put that to use. Consumer debt, like credit cards or higher interest car loans, eat into your cash flow with extremely high interest rates and should be paid off with haste. Take inventory of every debt you have – think credit cards, car payments, student loans, personal loans, etc.

Two popular methods for paying this off are ranking your debt in order of balance or by interest rate. Mathematically, paying off your highest interest rate loans first will net you the most gain. Emotionally however, knocking off your lowest balance account may keep your motivation higher as you continue to see progress. Finally, stack your money – as you pay off one account, put the money towards the next one on your list.

Plan your cash flow

Once that high interest debt is paid off, time to watch your savings grow! Create a few short, medium, and long term goals and put your cash flow towards those goals. Be sure to make sustainable and measurable goals like “I want to put $100 per month towards my down payment goal.”

Open a High Yield Savings Account

For real guys & gals – this is free money. Your typical savings account makes somewhere in the realm of 0.02% interest, for ease of discussion, let’s call that 0%. In today’s rate world, HYSA (High Interest Savings Accounts) can get you 5%+. It’s important to note that these rates fluctuate based on the federal rates determined by several economic factors. In short, it may not stay this high for too long. To put that into dollars, if you put your $10,000 emergency savings into an HYSA making 5%, you’d earn over $500 per year for doing nothing.

There are many HYSAs to choose from – NerdWallet does a great job keeping inventory of some of the highest rated – check that out here.

Check your credit score

Credit score, while quite confusing, is an important factor towards qualifying for loans on some of life’s biggest purchases. The interest rate that you qualify for on houses & automobiles are derived from your credit score. Many credit card or bank mobile apps offer some sort of credit journey where you can view your score & the factors that make it. If you’re really interested, heres an article that explains how your credit score is calculated.

Finally, you are entitled to view your credit report for free from all 3 credit agencies once per year. If a site is telling you that you have to pay to view your credit report, you’re not in the right place.

Optimize your credit card rewards

Credit cards can be a touchy subject. Some of us need to cut them up and pretend like they dont exist, but in most cases DO NOT CLOSE YOUR ACCOUNTS. We can all learn to use credit cards in a way that provides significant rewards for the spending that we were going to do anyways.

Credit cards offer rewards in a few different ways – sign on bonues and rewards per categories. Often times, you can find a mix of 2-3 credit cards and optimize your cash back opportunities so you are getting 3% – 5% back on nearly every dollar you spend. Again, NerdWallet keeps an awesome list of some of the best rewards based credit cards.

Consolidate your retirement accounts

If you’ve jumped around quite a bit in your career, you likely have multiple retirement accounts across multiple trustees and you don’t even know what you’re invested in. As a money coach, I can’t get into where you should invest your hard earned retirement money, but what I can say is: Employee sponsored retirement accounts typically have limited offerings and incur high fees. Consider consolidating your employee retirement funds into accounts with more offering and lower fees.

Celebrate your wins along the way

I am a huge proponent of celebrating your money wins – big or small. If you pay off your credit debt, CELEBRATE! Disclaimer: Don’t ball out too hard or you’ll end up right where you started!

Download your 2024 Money Guide

Want to follow these steps and create your own checklist? No need – download The 2024 Money Guide here and follow along. Let me know how you progress throughout the year!

Interested in finacial coaching?

Let’s Chat!

Hiring a financial coach can be a life changing experience, for the better. We offer 1:1 coaching focused on tracking your spending, optmizing cash flow, and building that money mindset that will last the rest of your life. Get in touch or learn more below!

{kind=link}